There’s a particular kind of regret that comes with estate planning mistakes, and it’s different from most. It doesn’t hit right away. It shows up nine months later when your family is still in the middle of a court process that should have been over in weeks, or when a sibling relationship quietly breaks under the weight of a dispute that a well-written trust document would have prevented entirely.

A family in Lakewood spent close to a year tangled up with the Jefferson County Probate Court after a father died without a trust. The house was modest, nothing dramatic, but it was in his name alone. No surviving spouse. One sibling with questions. Three attorneys were involved in the case for eleven months before anything was resolved. The estate wasn’t complicated. The situation was.

Probate and living trusts come up in the same conversation, but they’re not really competing options. Probate is a court process that handles your estate after you’re gone. A living trust is a structure you create now, so that process isn’t necessary. Which one matters for your family depends on specifics that no general article can fully answer, but a living trust attorney in Denver can.

What follows is what you need to understand going in.

What Probate Actually Is in Colorado

When someone dies, their financial life doesn’t just automatically sort itself out. If assets are held in their name alone and there’s no mechanism for automatic transfer, a court gets involved. That process is probate. It validates the will, settles unpaid debts, and oversees the handoff of whatever’s left.

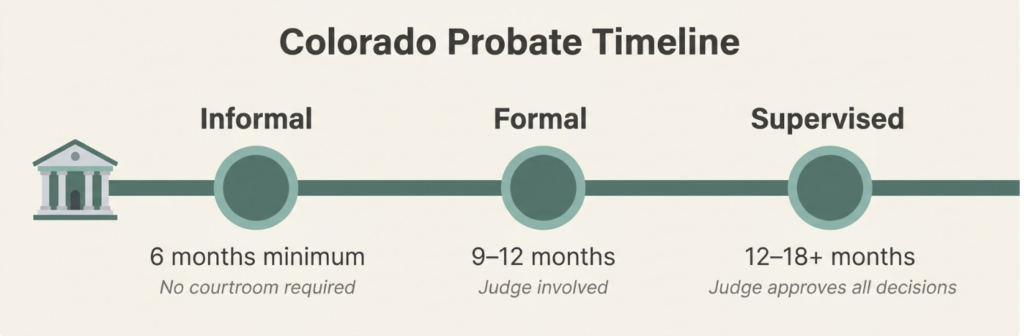

Colorado runs three different versions of it depending on the situation. Informal probate is the default when everything’s clean: a clear will, no disputes, a straightforward estate. No courtroom required; a registrar handles it. Formal probate brings a judge in when something’s being contested, whether that’s the will itself, a question about the deceased’s mental capacity, or a fight about who should be running the estate. Supervised probate is the most involved version, with a judge signing off on major decisions throughout the whole process rather than just at the opening.

Even the cleanest informal probate in Colorado requires patience. Creditors are legally entitled to a four-month window from the date of publication to file claims, meaning nothing is safely distributed until that clock runs out. In practice, just getting the estate open, waiting out the four months, and finalizing taxes means 6 to 12 months is the standard reality. And if there’s a disputed asset, a property in another state, or an appraisal question nobody can agree on, add more time.

Probate records are public. The filing goes to the courthouse, and anyone can look at it. Estranged relatives, creditors, and strangers. They can see the estate value and who got what. And the fees, court costs, attorney fees, and executor compensation all come out of the estate before the heirs see anything. In Colorado, that typically runs 3% to 7% of the estate’s total value. On a $500,000 estate, that’s $15,000 to $35,000 off the top.

What a Living Trust Does Differently

A revocable living trust is a legal document you create while you’re alive. Once set up and funded, it holds your assets and transfers them to your heirs upon your death, entirely outside the probate process. No court. No public record. No mandatory waiting.

The mechanic works like this: the trust legally owns the assets instead of you personally. When you die, there’s no personal estate to probate because the assets technically weren’t yours; they were the trust’s. Your successor trustee follows the instructions in the document and handles everything directly.

There’s also an irrevocable version. Once created, it’s mostly permanent; assets leave your estate entirely. That matters for Medicaid planning and certain creditor-protection strategies, but most Colorado families don’t start there.

Here’s where things go wrong more often than they should: a trust document that’s never funded does nothing. Every account, piece of property, and investment must be retitled in the trust’s name. A checking account still titled to John Smith personally goes through probate when John dies, trust document or not. This step, called funding the trust, is where many DIY estate plans quietly fail. The paperwork gets signed, everyone assumes it’s handled, and the actual transfers never happen.

Side-by-Side Comparison

|

Factor |

Probate |

Living Trust |

|

Timeline |

Six to 18 months |

Immediate to a few weeks |

|

Privacy |

Public record |

Private |

|

Cost |

Court fees + attorney (3%–7% of estate) |

Higher upfront setup ($1,500–$5,000+) |

|

Out-of-state property |

Ancillary probate required |

Avoided |

|

Incapacity control |

Risk of court-ordered conservatorship |

Seamless trustee handoff |

|

Contestability |

Easier to challenge |

Significantly harder to challenge |

When Probate Is Actually Fine

Not every situation calls for a trust, and the idea that probate is always the worst outcome is overblown. For many Colorado families, it’s manageable and maybe even the sensible default.

If most assets already have automatic transfer mechanisms, pay-on-death bank accounts, retirement accounts with named beneficiaries, jointly held property with survivorship rights, probate may apply to very little of what you’re actually leaving. A surviving spouse, adult children who aren’t going to dispute anything, and no real estate in just your name. In that scenario, setting up a trust might cost more than the probate it was designed to avoid.

Colorado also has a small estate affidavit process for qualifying estates. For deaths in 2026, the threshold is $88,000 in personal property (this adjusts periodically for inflation). Real estate is excluded regardless of value. Estates that qualify can skip full probate court entirely.

The point is: run the actual numbers for your situation before assuming you need a trust.

When a Living Trust Makes Real Sense for Colorado Families

Own real estate in more than one state? That’s not a Colorado probate problem; that’s a Colorado probate problem and an Arizona probate problem, or a Wyoming one, depending on where the property sits. Each state runs its own process. Two timelines, two sets of court filings, two legal bills. A trust handles all of it.

Blended family? A trust gives you specificity that a will can’t. You can set exact terms: which child gets what, at what age, under what conditions. A probate court interpreting a will has to work with whatever the document says, and wills are often far less precise than people assume when they’re writing them.

Privacy is something most people don’t think about until they realize their entire estate just became a public filing. For anyone in a visible role, anyone with assets that could attract unwanted attention, or anyone with a complicated family history, keeping the distribution private matters. Trusts don’t file anything with a court.

Incapacity is the issue that families consistently underestimate. If something happens before you die and you can no longer manage your own finances, a properly funded trust lets your successor trustee step in immediately. Without one, your family may need to go through a court-ordered conservatorship process just to pay your bills or manage your accounts.

And will contests, while rarer than people fear, are significantly harder to pull off against a trust. Trusts are private documents. Challengers have to prove something concrete: fraud, undue influence, or lack of capacity. And they often don’t even know the full terms of what they’d be challenging.

The Biggest Misconceptions About Trusts in Colorado

The most persistent one is that trusts are for wealthy people. They’re not. A retired teacher in Aurora who owns a rental property, has two stepchildren, and an estranged sibling has a stronger case for a trust than a wealthy person whose entire estate is in a joint account with a spouse and will pass directly with no court involvement. Wealth isn’t the variable. Complexity is.

Close behind that is the belief that a revocable trust reduces estate taxes. It doesn’t. The assets are still legally yours while you’re alive, so they’re still counted in your taxable estate. If estate tax reduction is an actual goal, that’s a different conversation involving entirely different trust structures, not a revocable living trust.

Then there’s the will situation. People assume that having a will means they’ve handled things. A will is the document that initiates probate. It tells the court what to do. It doesn’t remove the court from the process. Having one is important, but it’s not a substitute for trust if that’s what the situation actually calls for.

And finally, the fear of losing control. With a revocable trust, you’re typically serving as your own trustee during your lifetime. You manage assets exactly as you did before. You can sell property, change beneficiaries, move accounts, add assets, or dissolve the trust entirely if your circumstances change. Nothing shifts until you die or become incapacitated, which is when a transfer of control is appropriate anyway.

How to Decide Between Probate Planning and a Living Trust

- Do you own real estate in Colorado or anywhere else, titled in your name alone?

- Do you have minor children, a beneficiary with a disability, or someone who probably shouldn’t receive a large sum all at once?

- Is your family situation blended, with stepchildren, prior marriages, or any history that could create conflict during a distribution?

- Does the idea of your estate becoming a public court document after you die bother you?

- Could your family get through a 9- to 12-month probate process, financially and emotionally, without it causing serious harm?

Two or more yeses and a trust are probably worth exploring. A revocable living trust attorney in Colorado can review your specific asset picture and tell you clearly whether a trust saves your heirs money or just adds upfront costs with little return.

Conclusion: Choosing the Path That Protects Your Family

For clean, simple estates, probate is genuinely fine. For everyone else, especially families with real property, blended situations, privacy concerns, or a need for incapacity planning, a trust almost always makes more sense when you account for the full cost and timeline of both options.

The real issue isn’t which tool is theoretically better. It’s that most Colorado families who end up stuck in a difficult probate situation didn’t fail to plan carefully. They just never got around to planning. That gap between knowing you should deal with it and actually dealing with it is where most of the damage happens.

Summit Legacy Legal works with Colorado families from offices in Greenwood Village and Lakewood. A Colorado living trust built right today costs a fraction of what an avoidable probate process would run later.

Frequently Asked Questions About Probate and Trusts in Colorado

How long does probate take in Colorado?

Six months is the legal floor, and it doesn’t start until the estate is officially opened with the court. That window exists for creditors, not because the administrative work takes that long. Most real estate transactions close in nine to 18 months. A contested will, out-of-state assets, or a difficult appraisal can push it past the 2-year mark. Informal probate moves fastest. Formal and supervised proceedings don’t.

What does a living trust actually cost?

Attorney fees for a basic revocable living trust run $1,500 to $3,500 in most cases. A full plan with a pour-over will, power of attorney, and advance directive comes to $2,500 to $5,000 or more. That number looks different next to Colorado probate, which typically runs 3% to 7% of estate value. A $400,000 estate may lose $12,000 to $28,000 before heirs see a dollar. Trusts often pay for themselves.

Can I have a will and a trust at the same time?

Yes, and most complete estate plans include both. A pour-over will captures anything that didn’t make it into the trust and sends it through probate into the trust after death. It’s also the only document that can legally name a guardian for minor children. A trust can’t do that.

Revocable versus irrevocable: what’s the real difference?

Revocable means you can change or cancel it while you’re alive. Assets stay in your taxable estate. Irrevocable means it’s largely fixed once signed, and assets leave your estate entirely, which matters for Medicaid planning and some tax strategies. Most families in Colorado start with a revocable. Irrevocable comes into play when a specific planning goal requires it.

I have a trust. Do I still go through probate?

Not for what’s inside the trust. Anything left outside it, a forgotten account, a car still in your name, a property that never got retitled, can still end up in probate. That’s exactly what a pour-over will handle. Accounts with pay-on-death designations and retirement accounts with named beneficiaries skip both probate and the trust. They transfer directly.

What’s the small estate threshold in Colorado right now?

$80,000 in personal property for the most recent years; $86,000 for deaths in 2025 per the Colorado DMV. Adjusts annually. Real estate doesn’t qualify regardless. Estates under the threshold can use an affidavit to collect assets without opening full probate.

Can someone contest a living trust?

Technically, yes, but it’s a much harder case than contesting a will. The challenger has to prove fraud, undue influence, or lack of mental capacity at the time of signing. High bar. Add to that the fact that trusts are private documents, so outside parties often don’t even know enough about the terms to mount a meaningful challenge. Working with a revocable living trust attorney in Colorado to execute and fund the document correctly from the start is the most reliable defense.